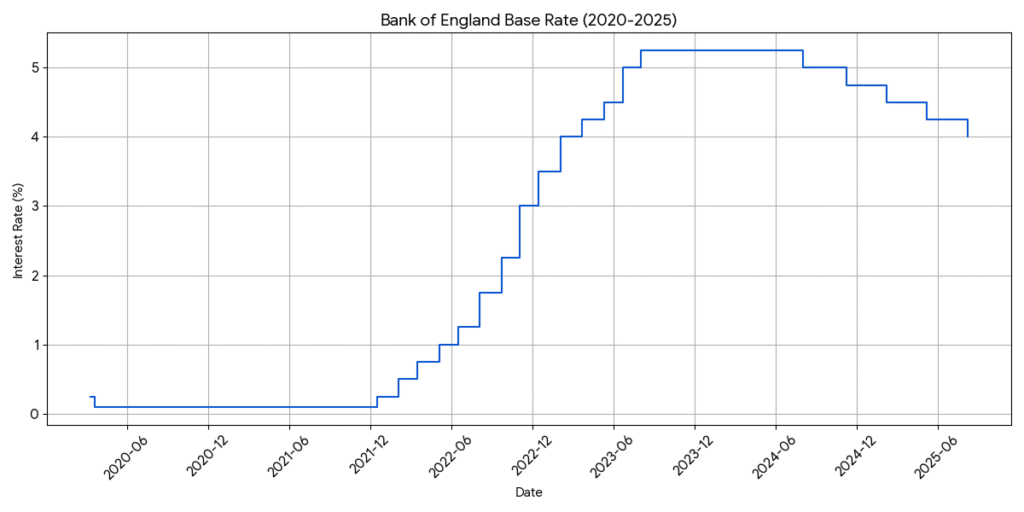

Today, the Bank of England cut its base rates from 4.25% to 4%.

This decision has some practical implications for the state of our personal finances, including those with a mortgage, savers, small businesses and job markets — and the health of the wider economy.

What exactly is the Bank of England base rate — and why does it matter?

The base rate is the interest rate the Bank of England charges high street banks (like Barclays, LBG, Monzo etc) when they borrow money. It’s not something you pay directly — but it influences almost every other interest rate in the economy. Think of it as the “reference rate” for how money is priced across the UK economy.

When the Bank raises the base rate, it becomes more expensive for banks to borrow, and they pass that cost on to us through higher mortgage rates, pricier loans and credit cards. When the Bank cuts it, borrowing becomes cheaper, encouraging more spending and investment — though usually at the cost of lower savings returns.

So while you never deal with the base rate directly, it affects your mortgage, your savings, your rent, your job security, and the prices you see in shops. It’s one of the biggest levers the Bank has to steer the economy — and to shape how easy or hard daily financial life feels.

Why is the Bank cutting now?

The BoE is responsible for managing inflation and interest rates – and after nearly two years of trying to get inflation under control, the Bank is facing a new problem: a weakening economy. Inflation is now back near the 2% target, but growth is slow, business investment is soft, retail spending has lost momentum, and unemployment is starting to creep up.

So, this rate cut is not about encouraging consumer spending. It’s about easing some of the pressure — helping lower the cost of borrowing for businesses and households, and giving the economy a bit more breathing space without reigniting inflation.

What this means for mortgage holders

The reduction in base rates would only impact mortgage holders who have a tracker (variable) rate mortgage. This is not a large group of people, as most mortgages taken out now are fixed – in fact about 90% of mortgages are fixed rate.

If you’re one of the 10% on a tracker or variable-rate mortgage, you’ll probably see a modest drop in your monthly payments. For example, someone paying £1,000 a month on their mortgage might now pay about £985 — a small but welcome £15 reduction of pressure. The exact amount depends on your mortgage size and terms, but the overall effect is a gentle shift in the right direction.

For people on fixed deals, the change isn’t immediate, but it matters. Lenders are already adjusting their expectations for where rates are headed. If your current fix is ending soon, you may start to see more affordable remortgage options. The worst of the rate spike appears to be behind us.

What it means for savers

When base rates fall, savings rates usually follow — and often quickly. If your easy-access account has been paying you 4.5% or more, don’t be surprised if that dips soon. Fixed-term bonds may hold steady for a little while longer, but they’re likely to drop too.

If you have savings on last year’s high rates, now is a good time to check in. Make sure your money is still earning a decent return — and be ready to move it if not.

There are still some decent savings rates available:

| Account Type | Provider(s) | Best Rates (AER) |

|---|---|---|

| Easy-access savings | Chase | 5.00% (MoneySavingExpert.com) |

| Notice (95-day) | RCI Bank UK | 4.70% (MoneySavingExpert.com) |

| Cash ISA (easy access) | Plum, Tembo, Moneybox | up to 4.66% (MoneyWeek) |

| 1-year fixed-rate bonds | LHV Bank, Vanquis, others | up to 4.50% (MoneyWeek) |

| 1-year fixed saver (Atom) | Atom Bank | 4.42% (atombank.co.uk) |

And what it means for the wider economy, jobs, investment, and stability

Beyond individual households, today’s cut is also aimed at shoring up the job market. With borrowing costs staying high for much of the past two years, businesses have been hesitant to invest or expand. Lower rates may help unlock some of that, particularly for smaller firms.

It’s also about confidence. This move won’t flip the economy overnight, but it sends a signal that the Bank is ready to support growth — not just contain prices.

What you should do now

If your mortgage is up for renewal, this is a good moment to reassess your options. Speak to a broker, understand what’s out there, and think carefully about whether to fix or stay flexible.

If you’re saving, don’t sleepwalk into a lower return. Rates are still good by historical standards — but they may not stay that way for long. Compare, switch, and make your cash work harder.

If you’re running a business, the environment may be marginally more supportive — but credit conditions are still tight, and resilience will matter.

Leave a Reply